Money management is a crucial skill that can make a significant difference in your financial life. It involves planning, saving, investing, and spending your money wisely. Whether you are trying to save for a big purchase, pay off debt, or simply ensure that you have enough money to live comfortably, good money management is essential. This article will guide you through the basics of money management, helping you take control of your finances with confidence.

What is Money Management?

Money management refers to the process of budgeting, saving, investing, and spending your money in a way that maximizes your financial well-being. It involves making informed decisions about how to allocate your resources to meet your needs and achieve your financial goals.

Why is Money Management Important?

Good money management is important because it:

- Helps You Save Money: By managing your money wisely, you can set aside funds for emergencies, future goals, and unexpected expenses.

- Reduces Financial Stress: When you have a clear plan for your finances, you are less likely to worry about money problems.

- Allows You to Achieve Financial Goals: Whether you want to buy a house, start a business, or retire comfortably, good money management can help you reach your goals.

- Prevents Debt: Effective money management helps you avoid unnecessary debt and manage any existing debt more efficiently.

Steps to Effective Money Management

Here are some simple steps to help you manage your money better:

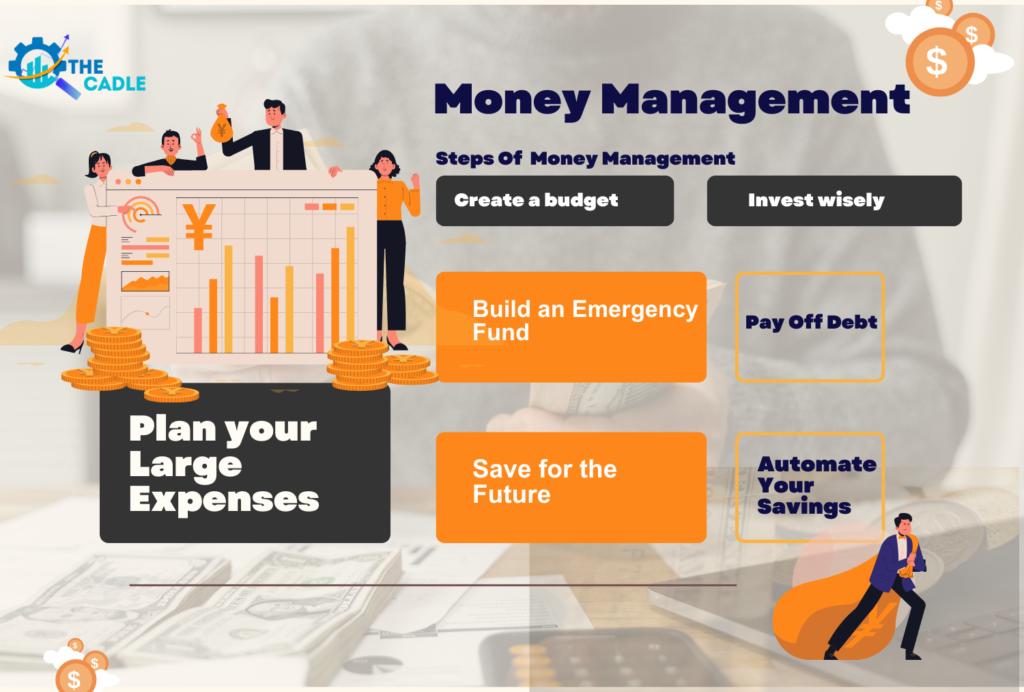

1. Create a Budget

A budget is a plan that outlines your income and expenses over a certain period, usually a month. It helps you see where your money is going and ensures that you are not spending more than you earn. To create a budget:

- List Your Income: Include all sources of income, such as your salary, bonuses, and any side income.

- List Your Expenses: Include fixed expenses (like rent and utilities) and variable expenses (like groceries and entertainment).

- Track Your Spending: Keep track of your spending to see if you are staying within your budget.

- Adjust as Needed: If you find that you are overspending, look for areas where you can cut back.

2. Build an Emergency Fund

An emergency fund is money set aside to cover unexpected expenses, such as medical bills or car repairs. Having an emergency fund can prevent you from going into debt when something unexpected happens. Aim to save at least three to six months’ worth of living expenses in your emergency fund.

3. Pay Off Debt

If you have debt, make paying it off a priority. Start by paying off high-interest debt first, such as credit card balances. You can use strategies like the debt snowball (paying off the smallest debts first) or the debt avalanche (paying off the highest interest debts first) to tackle your debt more effectively.

4. Save for the Future

Saving for the future is essential for achieving long-term financial goals, such as buying a house, sending your children to college, or retiring comfortably. Set aside a portion of your income each month for savings. Consider opening a separate savings account to keep this money safe and growing.

5. Invest Wisely

Investing is a way to grow your wealth over time. There are many different types of investments, such as stocks, bonds, and real estate. Before you invest, make sure you understand the risks and rewards of each type of investment. It’s also a good idea to diversify your investments to reduce risk.

6. Monitor Your Credit Score

Your credit score is a number that reflects your creditworthiness. It affects your ability to get loans, credit cards, and even rental agreements. To maintain a good credit score:

- Pay your bills on time.

- Keep your credit card balances low.

- Avoid opening too many new credit accounts at once.

Monitoring your credit score regularly can help you spot any errors or issues that could hurt your score.

Tips for Better Money Management

- Automate Your Savings: Set up automatic transfers from your checking account to your savings account to ensure you save consistently.

- Live Within Your Means: Avoid spending more than you earn by sticking to your budget and making mindful purchasing decisions.

- Plan for Large Expenses: If you know you have a large expense coming up, start saving for it ahead of time to avoid financial strain.

- Review Your Finances Regularly: Take time each month to review your budget, track your spending, and assess your financial goals.

Common Money Management Mistakes to Avoid

- Not Having a Budget: Without a budget, it’s easy to lose track of your spending and overspend.

- Failing to Save: If you don’t prioritize savings, you may find yourself unprepared for emergencies or unable to reach your financial goals.

- Ignoring Debt: Ignoring your debt won’t make it go away. Make a plan to pay it off as soon as possible.

- Living Beyond Your Means: Spending more than you earn can lead to debt and financial stress.

The Role of Financial Planning in Money Management

Financial planning is a critical component of effective money management. It involves setting short-term and long-term financial goals, creating a strategy to achieve them, and regularly reviewing and adjusting your plan as needed. Here’s how financial planning can enhance your money management efforts:

1. Setting Clear Financial Goals

Setting specific, measurable, achievable, relevant, and time-bound (SMART) goals gives you a clear direction and purpose for your money management efforts. These goals can include saving for a vacation, buying a car, paying off debt, or building a retirement fund.

- Short-Term Goals: These are goals you plan to achieve within the next year, such as saving for a holiday or paying off a small debt.

- Long-Term Goals: These goals are typically set for five or more years in the future, such as buying a home or saving for retirement.

2. Creating a Financial Plan

A financial plan is a comprehensive roadmap that outlines how you will achieve your financial goals. It includes your budget, savings strategy, investment plan, and debt repayment plan. A well-crafted financial plan considers your current financial situation, future aspirations, and risk tolerance.

- Budgeting: A budget is the foundation of any financial plan. It helps you allocate your income to various expenses and savings goals, ensuring that you stay on track.

- Saving: Your financial plan should include a strategy for saving money regularly. This might involve setting up automatic transfers to a savings account or contributing to a retirement fund.

- Investing: If you have long-term goals, such as retirement, investing is a crucial part of your financial plan. Consider speaking with a financial advisor to determine the best investment strategy for your goals.

3. Regularly Reviewing Your Financial Plan

Financial planning is not a one-time task. Your financial situation and goals may change over time, so it’s important to review and adjust your financial plan regularly. This ensures that your money management strategy remains aligned with your current needs and future aspirations.

Tools and Resources for Effective Money Management

Managing your money effectively can be made easier with the right tools and resources. Here are some that can help:

1. Budgeting Apps

Budgeting apps can simplify the process of tracking your income and expenses. Many apps allow you to set up a budget, categorize your spending, and monitor your progress in real-time. Some popular budgeting apps include:

- Mint: A free app that connects to your bank accounts, tracks your spending, and helps you create a budget.

- YNAB (You Need a Budget): A paid app that helps you allocate every dollar you earn and stay within your budget.

- PocketGuard: A free app that shows how much disposable income you have after paying your bills and setting aside savings.

2. Savings Calculators

Savings calculators can help you determine how much you need to save each month to reach your financial goals. These tools take into account your current savings, interest rates, and the time frame for your goals.

3. Investment Platforms

If you’re new to investing, online investment platforms can provide an easy way to start. Many platforms offer educational resources and tools to help you choose investments that align with your goals and risk tolerance. Some popular investment platforms include:

- Robinhood: A user-friendly platform that allows you to trade stocks, ETFs, and cryptocurrencies without paying commissions.

- Betterment: A robo-advisor that creates a personalized investment portfolio based on your financial goals.

- Vanguard: Known for its low-cost index funds, Vanguard offers a range of investment options for both beginners and experienced investors.

4. Financial Literacy Resources

Improving your financial literacy can significantly enhance your money management skills. Many free resources are available online, including articles, videos, podcasts, and courses. Some recommended resources include:

- Investopedia: A comprehensive resource for learning about finance, investing, and money management.

- The Financial Diet: A website and YouTube channel that offers practical advice on budgeting, saving, and managing money.

- Khan Academy: Offers free courses on personal finance and investing.

The Psychological Aspect of Money Management

Understanding the psychological aspect of money management is crucial for long-term success. Your attitudes, beliefs, and emotions about money can influence your financial decisions and behaviors.

1. Understanding Your Money Mindset

Your money mindset refers to your beliefs and attitudes about money. It can be shaped by your upbringing, experiences, and culture. For example, some people may view money as a source of security, while others may see it as a means to enjoy life. Understanding your money mindset can help you identify any negative beliefs or habits that may be hindering your financial success.

2. Overcoming Emotional Spending

Emotional spending occurs when you buy things to cope with emotions such as stress, boredom, or sadness. While it may provide temporary relief, emotional spending can lead to financial problems in the long run. To overcome emotional spending:

- Identify Triggers: Recognize the emotions or situations that trigger your spending.

- Find Alternatives: Instead of spending money, find healthier ways to cope with your emotions, such as exercising, meditating, or talking to a friend.

- Create a Spending Plan: Plan your purchases in advance and stick to your budget.

3. Developing Healthy Money Habits

Developing healthy money habits is key to successful money management. These habits can include:

- Paying Yourself First: Prioritize saving by setting aside a portion of your income as soon as you get paid.

- Living Below Your Means: Spend less than you earn to ensure you have money left over for savings and investments.

- Tracking Your Progress: Regularly monitor your financial progress to stay motivated and on track.

The Importance of Financial Discipline

Financial discipline is the ability to control your spending and stick to your financial plan, even when it’s challenging. It requires self-control, patience, and a commitment to your financial goals.

1. Sticking to Your Budget

Sticking to your budget is one of the most important aspects of financial discipline. This means resisting the temptation to overspend, even when it’s difficult. To make it easier:

- Set Realistic Goals: Make sure your budget is realistic and achievable, so you’re more likely to stick to it.

- Reward Yourself: Give yourself small rewards for sticking to your budget, such as treating yourself to a movie or a nice meal.

2. Avoiding Impulse Purchases

Impulse purchases can quickly derail your budget and financial plan. To avoid them:

- Wait Before You Buy: If you see something you want, wait 24 hours before making the purchase. This gives you time to decide if you really need it.

- Make a Shopping List: Before you go shopping, make a list of what you need and stick to it.

- Set Spending Limits: Set a limit for how much you can spend on non-essential items each month.

3. Staying Committed to Your Financial Goals

Staying committed to your financial goals requires discipline and focus. To stay motivated:

- Visualize Your Goals: Imagine what it will feel like to achieve your financial goals, whether it’s being debt-free, owning a home, or retiring comfortably.

- Track Your Progress: Keep track of your progress towards your goals, and celebrate your successes along the way.

- Seek Support: Share your financial goals with a friend or family member who can provide encouragement and accountability.

Effective money management is essential for achieving financial stability and success. By creating a budget, building an emergency fund, paying off debt, saving for the future, and investing wisely, you can take control of your finances and work towards your financial goals. Remember, financial planning, discipline, and a positive money mindset are key components of successful money management. Start implementing these strategies today, and you’ll be well on your way to a secure and prosperous financial future.